About Enea Group

ENEA Group is a vice-leader of the Polish power market as regards electricity. It manages the complete value chain on the electricity market: from fuel, through electricity generation, distribution, sales and Customer service.

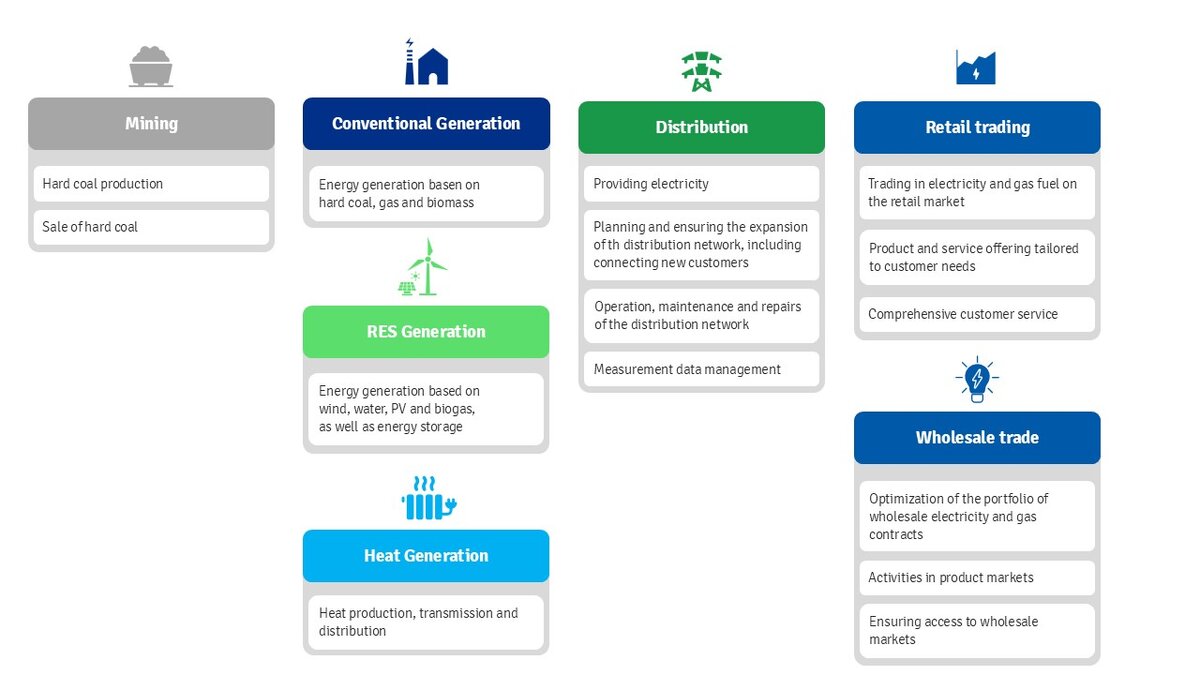

The Enea Group operates in the following business areas: Production, Conventional Power Generation, Renewable Energy and Heat Generation, Distribution and Trading (broken down into two segments: retail trading and wholesale trading). There are 8 leading entities in the Enea Group, namely Enea S.A. (trading in electricity), Enea Operator sp. z o.o. (distribution of electricity), Enea Wytwarzanie sp. z o.o., Enea Elektrownia Połaniec S.A. and Enea Nowa Energia sp. z o.o. (generation and sales of electricity), Enea Trading sp. z o.o. (wholesale of electricity), Enea Ciepło sp. z o.o. (generation and sales of heat and electricity) and LW Bogdanka S.A. (coal mining).

Enea Group's business areas

ENEA Group in numbers

Enea Group Structure